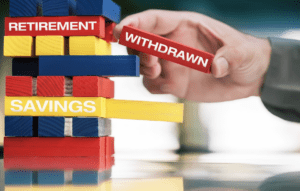

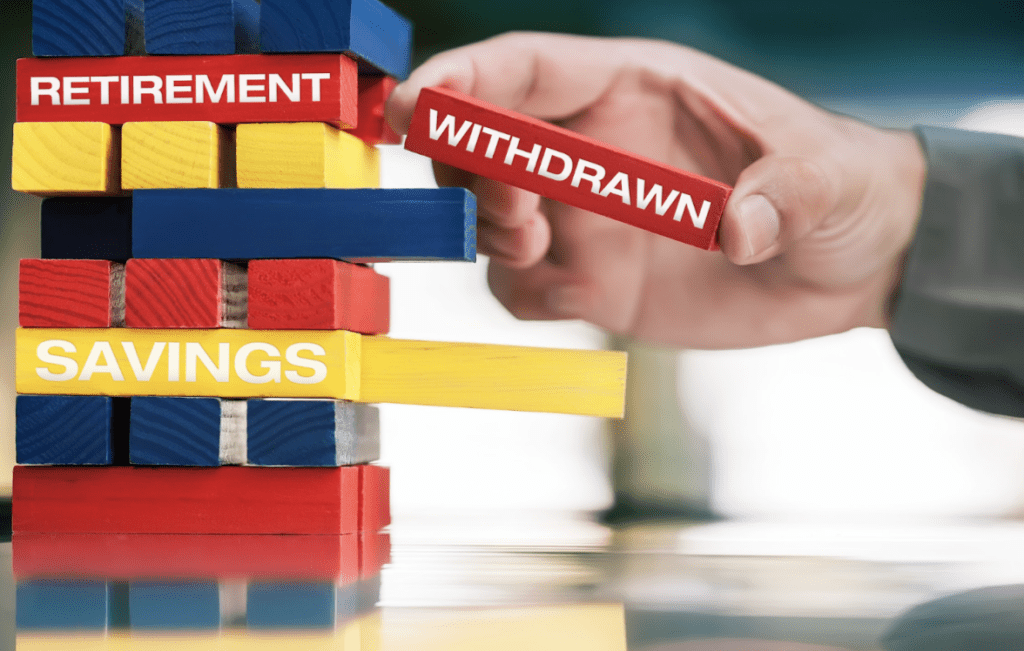

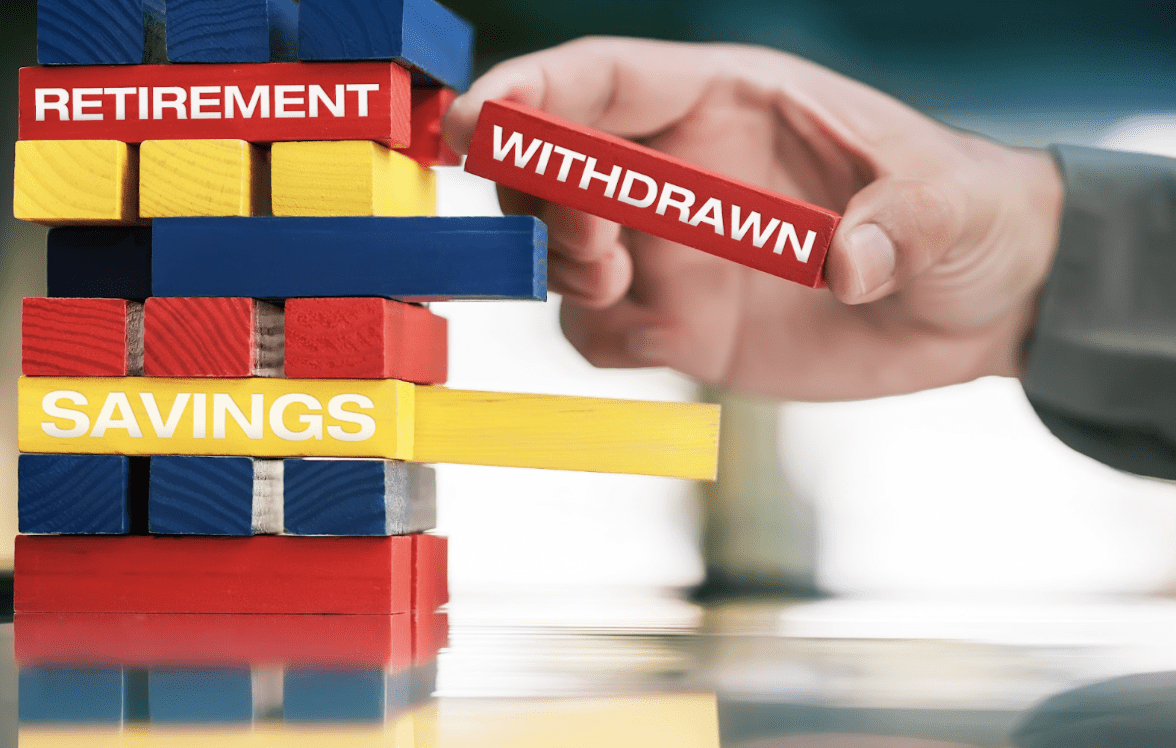

Navigating the many ins and outs of retirement withdrawals can be a complex process, especially when it comes to minimizing taxes and avoiding penalties. At Streetlight Financial we understand the importance of making informed decisions that maximize your retirement income. In this blog, we’ll delve into practical strategies for retirement withdrawals, helping you retain more of your hard-earned savings.

1. Understanding Retirement Withdrawal Strategies

Optimizing Withdrawals for Tax Efficiency

When it comes to retirement withdrawals, timing and source are key factors that can significantly impact your tax liability. A common strategy is to withdraw first from taxable accounts, then tax-deferred accounts, and finally, Roth accounts, where withdrawals are usually tax-free. This allows tax-deferred or already taxed assets to potentially grow over a longer period.

However, a more balanced approach might involve proportional withdrawals, distributing your retirement income evenly across different account types. This strategy can lead to a more stable tax bill over your retirement years. A Registered Representative can help you navigate which sequence of withdrawals makes the most sense for your situation.

2. Navigating Age-Related Considerations and Rules

Avoiding Early Withdrawal Penalties

One crucial aspect of managing withdrawals in retirement is understanding age-related rules and penalties. For instance, withdrawing funds from certain retirement accounts before age 59½ generally incurs a 10% penalty. Therefore, planning your withdrawals to start at the right age is essential to avoid these penalties.

Required Minimum Distributions (RMDs)

After reaching age 72, you are required to start taking Required Minimum Distributions (RMDs) from your retirement accounts like 401(k)s and traditional IRAs. Failure to comply with RMD rules can result in hefty penalties – up to 50% of the amount that should have been withdrawn. Planning for these distributions and understanding their impact on your taxes is crucial for effective retirement planning.

3. Leveraging Tax-Diversification Strategies

Balancing Different Account Types

A diversified retirement portfolio isn’t just about a mix of stocks and bonds; it also involves diversifying across different types of tax-advantaged accounts. By having a combination of account registrations, you gain more flexibility to manage your retirement withdrawals in a tax-efficient manner.

Understanding Roth Conversions

Consult with your Registered Representative on the strategy of Roth IRA conversions, where you convert a portion of your tax-deferred savings into a Roth IRA. This move requires paying taxes upfront but can result in tax-free withdrawals later, which could be beneficial depending on your future tax situation.

4. Planning for the Long-Term

Forecasting Your Retirement Needs

Accurately projecting your annual retirement expenses is critical. It helps in determining a sustainable withdrawal rate that preserves your savings while meeting your needs. The commonly suggested withdrawal rate is 4% to 5% of your retirement savings annually, adjusted for inflation. However, this rate might vary based on your specific circumstances and market conditions.

Consulting with a Tax Professional

Engaging with a tax advisor and a financial planner can provide tailored advice, especially when dealing with complex scenarios. They can help in devising a withdrawal strategy that aligns with your financial goals and tax situation.

5. Conclusion: Smart Planning for Retirement Withdrawals

In conclusion, managing retirement withdrawals requires a thoughtful approach that considers various factors like tax implications, account types, and personal retirement goals. By employing strategies like understanding withdrawal sequences, balancing different account types, and staying aware of age-related rules, you can effectively reduce tax liabilities and avoid penalties. Remember, each retirement journey is unique, and your withdrawal strategy should reflect your personal financial landscape. With careful planning and professional advice, you can ensure a financially secure and fulfilling retirement.

Contact Us! We Understand Finance And Trust.

Our Streetlight Financial Offices in Massachusetts and Vermont.